How to Move Up from a Starter Home in Berks County: 2026 Success Guide

Who's This For? Current Berks County homeowners, particularly those in starter homes (Reading, Kutztown, etc.) who are ready to upgrade to larger properties in premium school districts like Wyomissing Area or Wilson, seeking strategies to manage simultaneous selling and buying.

Table of Contents

Thinking about upgrading from your starter home in Berks County?

Thousands of homeowners reach this stage every year—but most don’t know how to time their sale, manage equity, or secure their next home without risking two mortgages. This guide reveals the smartest 2025 move-up strategies, financing options, and step-by-step plans used by successful Wyomissing, Sinking Spring, and Reading homeowners.

Move-Up vs Staying in Your Starter Home (2025 Comparison)

| Starter Home | Move-Up Home |

|---|---|

| Limited space, fewer bedrooms | More space for growing families |

| Lower equity growth potential | Higher long-term appreciation |

| Often outside top districts | Access to top Berks County schools |

| Minimal upgrade options | Updated kitchens, baths & amenities |

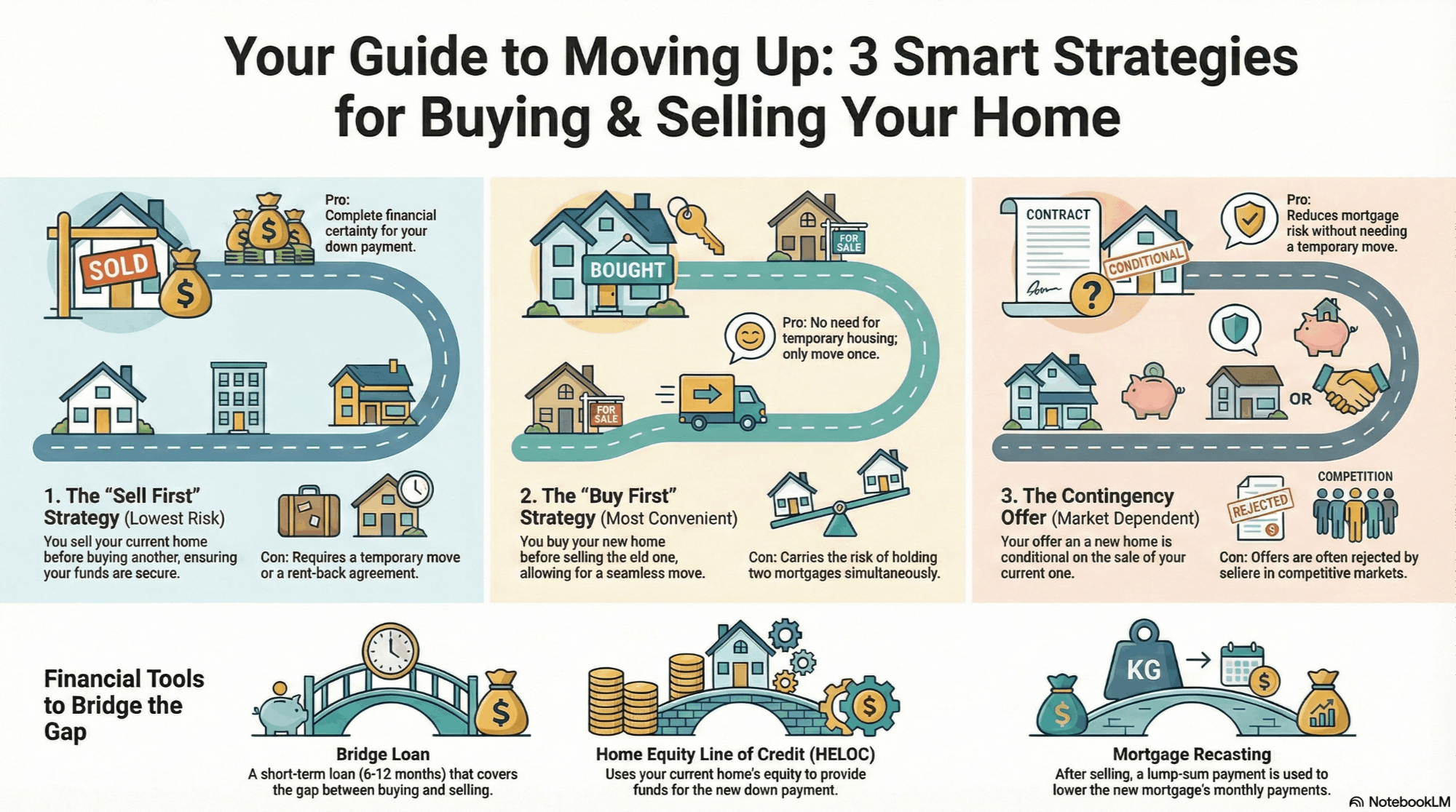

The 3 Essential Strategies for a Smooth Move-Up

Moving from one home to another involves complex coordination, especially in a competitive market like Berks County. These three common strategies help mitigate the financial risk of holding two mortgages simultaneously.

1. The "Sell First" Strategy (Least Risk)

This approach ensures you have your down payment and closing costs secured before making an offer on a new property.

- How it works: You list and sell your current home, close, and then use the proceeds to purchase your next home. You may need a short-term rental or a pre-negotiated **rent-back agreement** with the buyer of your starter home.

- Best for: Homeowners who want to maximize their equity gain, minimize financial risk, and are comfortable with a temporary housing solution.

- Pro: Complete financial certainty on your down payment.

- Con: Requires a temporary move (or rent-back) while searching for the new home.

2. The "Buy First" Strategy (Most Convenience)

This method provides the convenience of moving into your new home before you have to move out of the old one, but it involves more financial complexity.

- How it works: You secure financing (often using a bridge loan or HELOC, see below) to purchase the new home. Once you move, you quickly list and sell the old home to pay off the interim financing.

- Best for: Families who cannot move twice or need the time to renovate the new home before moving in.

- Pro: Seamless transition and only one physical move.

- Con: Carries the risk of holding two mortgages if the starter home takes longer to sell.

3. The Contingency Offer (Market Dependent)

This strategy involves finding a new home and making an offer conditional on the sale of your current home.

- How it works: Your offer includes a **"Sale of Home" contingency**. If accepted, you have a set period (e.g., 30-60 days) to sell your starter home.

- Best for: Homeowners in a **balanced** market. This strategy is difficult in seller's markets like Wyomissing or Sinking Spring, where sellers often prefer non-contingent offers.

- Pro: Reduces the risk of two mortgages without needing temporary housing.

- Con: Sellers often reject contingent offers in competitive Berks County neighborhoods.

💰 Smart Financing Options for the Move-Up Buyer

Managing the timing of your equity transfer is the biggest hurdle. These financing tools help bridge the gap between closing dates.

1. Bridge Loans

A specialized short-term loan secured by your current home (or sometimes both homes). It literally "bridges" the period between buying the new home and receiving the proceeds from the sale of the old one.

- Timeline: Typically 6 to 12 months.

- Cost: Higher interest rates than a traditional mortgage, but the cost is temporary.

2. Home Equity Line of Credit (HELOC)

If you have significant equity in your starter home, a HELOC can provide access to funds for the down payment on the new home.

- Benefit: You only pay interest on the money you use, and you can pay off the balance immediately upon the sale of your starter home.

- Requirement: Requires good credit and ample equity.

3. Recast Your New Mortgage

If you close on the new home before selling the old one, you can make a large lump-sum payment (from your sale proceeds) shortly after closing. Many lenders allow you to **recast** the new mortgage, adjusting the principal balance and lowering your monthly payment without a full refinance.

Ready to Move Up?

The success of your move-up plan depends heavily on local market expertise and timing. Consulting with a Berks County specialist can help you determine the optimal strategy—Sell First vs. Buy First—based on the current average time-on-market for homes in your neighborhood and the target area.

Would you like to explore the **average time-on-market** for a starter home in your specific Berks County town (e.g., Wyomissing, Sinking Spring, or Reading) to help choose the best strategy?

Categories

Recent Posts